The Hexis Nicotine Transition Score (HNTS) is our proprietary framework for assessing industry transition from combustible tobacco to safer nicotine products, commonly referred to as Reduced Risk Products (RRPs). We aim to capture not only a company’s progress to date, but also its RRP growth potential and commitment to transformation in a responsible and sustainable way.

The HNTS score for each company with exposure to combustible tobacco forms the basis for our engagement with them, and also informs the growth assumptions we use in our valuation models.

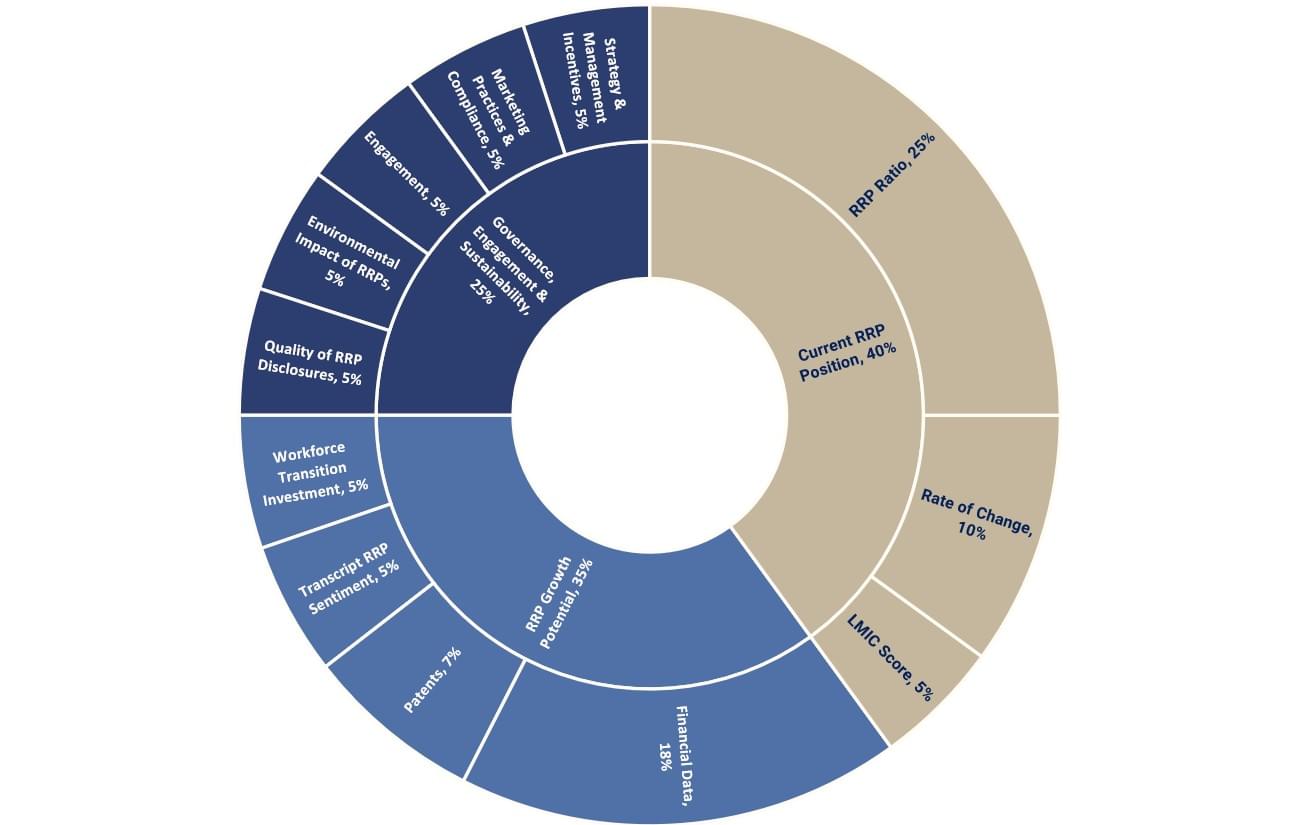

In building each company’s HNTS, we evaluate 27 indicators and 13 sub-indicators. AI, supervised and calibrated by our research team, is used extensively for scoring 11 of these indicators.

The 27 indicators are grouped into three categories and 12 sub-categories:

- Current RRP Position – 40% HNTS weighting

- RRP Growth Potential – 35%

- Governance, Engagement & Sustainability – 25%

HNTS Category and Sub-Category Weightings

Source: Hexis Capital Management

Our starting point is each company’s Current RRP Position, which accounts for 40% of the HNTS and consists of:

- The RRP contribution to sales in the most recent financial year (25%), taking into account both sales volumes and value,

- 2-year RRP momentum (10%) for both sales value and volumes

- RRP activities in low- and middle-income countries (LMICs), including the company’s hiring and patent activities in LMICs.

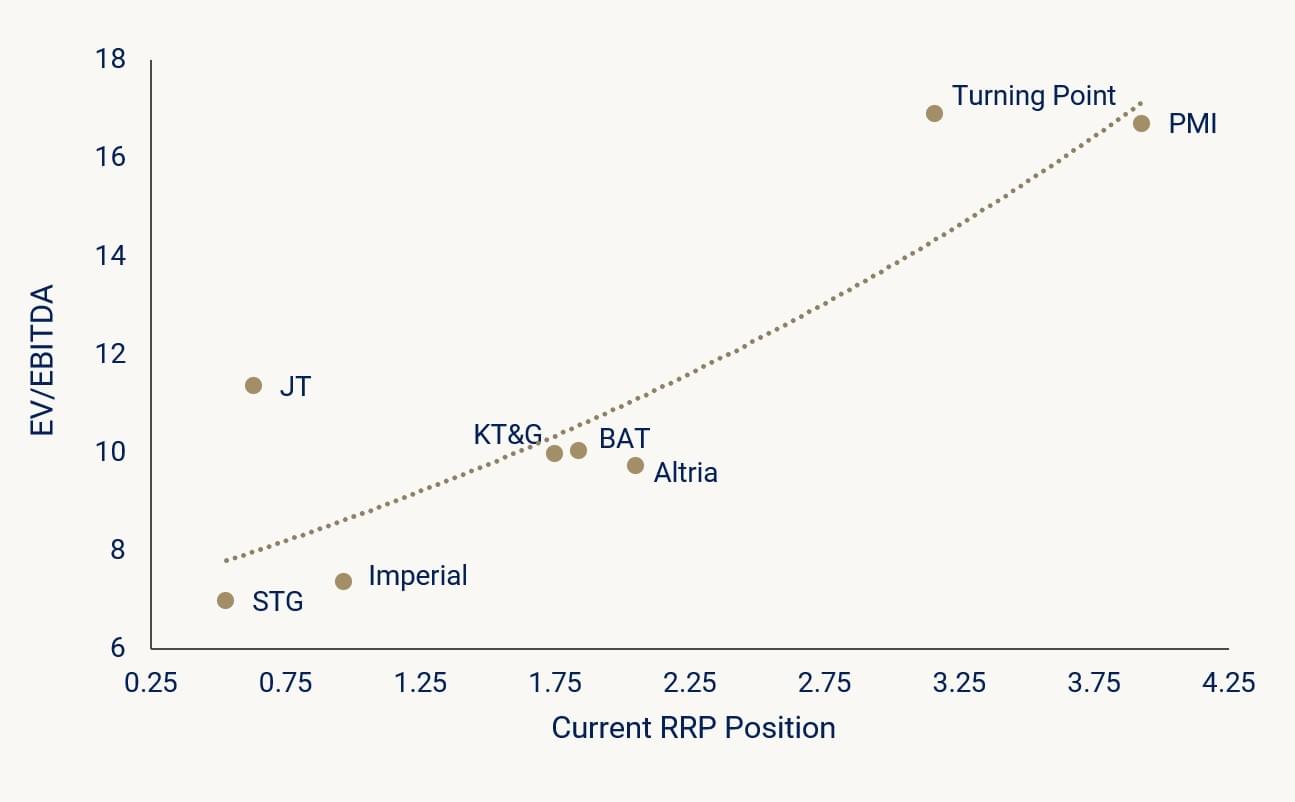

A tobacco company’s current RRP position, as defined by this measure, appears to be an important driver of its stock valuation and supports the economic argument for transformation.

Valuation v. HNTS – Current Position

Source: Bloomberg, HNTS Scorecard

Pricing date is 19-Jan-25

From an investor’s perspective, however, what ultimately influences future valuations is a company’s projected RRP position, rather than its current one. RRP Growth Potential accounts for 35% of the HNTS and comprises financial indicators focused on investment in RRPs, as well as sentiment analysis of company conference calls.

The category consists of:

- Company Financial Data (17.5%) – R&D, Capex and M&A directed at RRPs

- Patents (7%) – AI analysis and categorization of tens of thousands of patent filings. We view RRP patent filings as a potential long-lead indicator of future growth potential.

- Workforce Transition Investment (5.25%) – AI scraping and categorization of company job postings as a measure for workforce investment in RRPs.

- Transcript RRP Sentiment (5.25%) – AI is utilized to analyze and score RRP sentiment from company results conference calls.

Underpinning the two commercial elements of the HNTS is our assessment of Governance, Engagement and Sustainability, which contributes 25% to the HNTS.

We evaluate five equally weighted sub-categories:

- Strategy & Management Incentives (5%) - Commitment to harm reduction and governance structure for transition.

- Marketing Practices & Compliance (5%) - Assessment of youth prevention policies and disclosure of policy compliance and measures taken to prevent irresponsible marketing practices.

- Engagement (5%) – Company responses to engagement by the Fund and documented actions taken as a result of engagement.

- Environmental Impact of RRP Supply Chain and Products (5%) - Investment in sustainable RRP manufacturing, reduction in RRP production carbon footprint.

- Quality of RRP Disclosures (5%) – Quality of RRP disclosures.

HNTS-Enhanced Discounted Cash Flow (DCF) Valuation

We employ a three-stage DCF model to value our universe of stocks, which consists of tobacco companies with at least 1% of revenue from RRPs in their most recent 12-month reporting period, and non-tobacco companies that focus predominantly on RRPs.

High-Risk Products (HRPs), such as cigarettes, are in persistent, long-term decline, in much the same way that the arrival of cigarettes consigned pipe tobacco and chewing tobacco, the dominant forms of consumption at the time, to being niche categories. Global cigarette volumes have been falling for more than 15 years, with industry revenue growth being driven by price increases. The ability to grow revenues through price increases will likely dissipate over time as demand elasticity to price accelerates. Investors typically assume modest interim and negative terminal growth for pure-play HRP businesses.

In contrast, Reduced-Risk Products (RRPs), such as vapes, heated tobacco, and nicotine pouches, have grown at a CAGR of more than 25% over the past 10 years and are forecast to grow at 8-10% p.a. over the next five years. As a long-term sustainable industry, it would not be unreasonable to assume terminal growth in line with other consumer staples stocks.

In our valuation model, we assume consensus estimates for Stage 1 (years 1-3).

For Stage 2, individual company interim growth rates are informed by their HNTS and assumed Risk Category growth rates. A company at the low end of the HNTS spectrum will have an interim growth rate closer to HRPs, and those at the high end will have interim growth rates closer to RRPs.

For the calculation of terminal values (Stage 3 of the model), individual company terminal growth rates are informed by their HNTS and assumed Risk Category growth rates. A company at the low end of the HNTS spectrum will have a terminal growth rate closer to HRPs, and those at the high end will have terminal growth rates closer to RRPs

| HNTS ENHANCED DCF VALUATION | |||

| 3 Stage DCF Model | Stage 1: Years 1-3 | Stage 2: Years 4-10 | Stage 3: Terminal Value |

| Cash flow Drivers | Bloomberg Consensus Estimates | Interim Growth rate | Terminal Growth Rate |

| HNTS Adjustments | None | Individual company interim growth rates are informed by their HNTS and assumed Risk Category growth rates. At the extreme ends of the HNTS spectrum, a company with an HNTS of 0 will have an interim growth rate in line with HRPs, and one with a HNTS of 5 will have an interim growth rate in line with RRPs. | Individual company terminal growth rates are informed by their HNTS and assumed Risk Category growth rates. At the extreme ends of the HNTS spectrum, a company with an HNTS of 0 has a terminal growth rate in line with HRPs, and one with a HNTS of 5 has a terminal growth rate in line with RRPs. |

An investor should consider the investment objectives, risks, and charges and expenses of the fund carefully before investing. A prospectus which contains this and other information about the fund may be obtained by calling 1-800-617-0004, or by clicking here. The prospectus should be read carefully before investing.

Investing involves risk. Principal loss is possible. The Fund is a recently organized entity, giving prospective investors a limited track record on which to base their investment decision. The Fund’s investments will be concentrated in the securities of issuers in the tobacco, or nicotine - related group of industries. The tobacco industry is subject to significant risks and uncertainties that could materially and adversely affect the financial condition and cash flows, of companies operating in it. Investing in foreign securities typically involves more risks than investing in U.S. securities, and includes risks associated with: (i) internal and external political and economic developments – e.g., the political, economic and social policies and structures of some foreign countries may be less stable and more volatile than those in the U.S. or some foreign countries may be subject to trading restrictions or economic sanctions; (ii) trading practices – e.g., government supervision and regulation of foreign securities and currency markets, trading systems and brokers may be less than in the U.S.; (iii) availability of information – e.g., foreign issuers may not be subject to the same disclosure, accounting and financial reporting standards and practices as U.S. issuers; (iv) limited markets – e.g., the securities of certain foreign issuers may be less liquid (harder to sell) and more volatile; and (v) currency exchange rate fluctuations and policies. Investment in emerging market securities involves greater risk than that associated with investment in securities of issuers in developed foreign countries.

Derivatives may pose risks in addition to and greater than those associated with investing directly in securities, currencies or other investments, including risks relating to leverage, imperfect correlations with underlying investments or the Fund’s other portfolio holdings, high price volatility, lack of availability, counterparty credit, liquidity, valuation and legal restrictions. A total return swap is a contract in which one party agrees to make periodic payments to another party based on the change in market value of the assets underlying the contract, which may include a specified security, basket of securities, or securities indices during the specified period, in return for periodic payments based on a fixed or variable interest rate or the total return from other underlying assets. The Fund is a non-diversified, investment company under the 1940 Act. Because the Fund is non-diversified, it will invest a greater percentage of its assets in the securities of a limited number of issuers. Investing in medium and small capitalization companies may involve special risks because those companies may have narrower product lines, more limited financial resources, fewer experienced managers, dependence on a few key employees, and a more limited trading market for their stocks, as compared with larger companies. The securities of micro-cap companies may be more volatile in price, have wider spreads between their bid and ask prices, and have significantly lower trading volumes than the securities of larger capitalization companies.

ETFs are subject to risks that the market price of an ETF's shares may trade at a premium or discount to its net asset value, an active secondary trading market may not develop or be maintained, or trading may be halted by the exchange in which they trade, which may impact an ETF's ability to sell its shares. Shares of any ETF are bought and sold at market price (not NAV) and are not individually redeemed from the ETF. Brokerage commissions will reduce returns

The Hexis Active Nicotine Engagement ETF is distributed by Quasar Distributors, LLC

Definitions used on these pages:

R&D: Research and development spend – investment in developing new products, technologies, or capabilities.

M&A: Mergers and acquisitions spend – spending on acquiring or merging with other companies to expand scale, capabilities, or market access.

Capex: Capital expenditure – investment in long-term physical or intangible assets such as facilities, equipment, or infrastructure.

Discounted Cash Flow (DCF) model – a valuation method that estimates a company’s value by discounting its expected future cash flows back to today.

Terminal value – the estimated value of a business beyond the explicit forecast period in a DCF model.

Terminal growth rate – the assumed long-term, steady growth rate used to calculate terminal value.

EV: Enterprise Value – a measure of a company’s total value, calculated as market capitalisation plus net debt

EBITDA: Earnings before interest, taxes, depreciation and amortisation